Recent Academic Research

Website cookie tracking, social media sentiment, India's monsoon season, and a new execution method.

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Cookie Tracking and Sales Guidance

Firms that track users through website cookies develop a sharper internal picture of their operations, leading them to issue more frequent and higher-quality sales forecasts.

We often think of website cookies simply as tools for annoying targeted ads, but this research reveals they act as a vital data feed for corporate finance teams.

By capturing granular, real-time behavior from millions of users, cookies provide managers with an information edge that traditional accounting reports often miss. The study found that companies with higher cookie volume aren’t just better at marketing; they are significantly more likely to provide voluntary sales guidance to the public.

This relationship is particularly strong when the firm has the “data analytic technology” required to actually process that mountain of raw digital footprints into actionable insights.

However, this transparency has its limits, as managers tend to hold back these insights when industry competition is fierce or when strict privacy laws like the CCPA restrict their data collection. As the author notes, “the study highlights the role of firm-collected consumer data in shaping accounting information environments.”

Liu, Junhao, Website Cookies and Voluntary Disclosure (March 11, 2026). Journal of Accounting and Economics, Forthcoming, Available at SSRN: https://ssrn.com/abstract=6389578 or http://dx.doi.org/10.2139/ssrn.6389578

ML Straddle Strategy

Execution mechanism design can be as important as prediction accuracy for trading strategy performance.

This study challenges the common obsession with building “perfect” forecasting models by showing that how you trade matters just as much as what you predict. The researchers developed a “straddle-then-reveal” framework where a trader enters both long and short positions simultaneously at the market open.

At the end of the day, a machine learning model predicts the next day’s direction and designates one leg as “kept” and the other as “wrong”. Instead of simply closing the wrong leg, they use a “patient trader” approach, placing limit orders at a specific buffer from intraday price extremes to capture profits from the natural daily price range.

Remarkably, this buffer mechanism allows even incorrect predictions to be profitable “rescued” when the wrong leg exits near a daily high or low before the market reverses. Testing across 48 global securities, the strategy achieved universal outperformance with win rates as high as 85%. According to the authors, “execution mechanism design can amplify returns substantially beyond what prediction accuracy alone would suggest.”

González Maiz Jiménez, Jaime and López-Herrera, Francisco and Reyes-Santiago, Adán, Machine Learning Straddle Strategy with Buffer-Based Execution: A Patient Trader Approach to Equity Trading. Available at SSRN: https://ssrn.com/abstract=6401038 or http://dx.doi.org/10.2139/ssrn.6401038

Social Media Sentiment

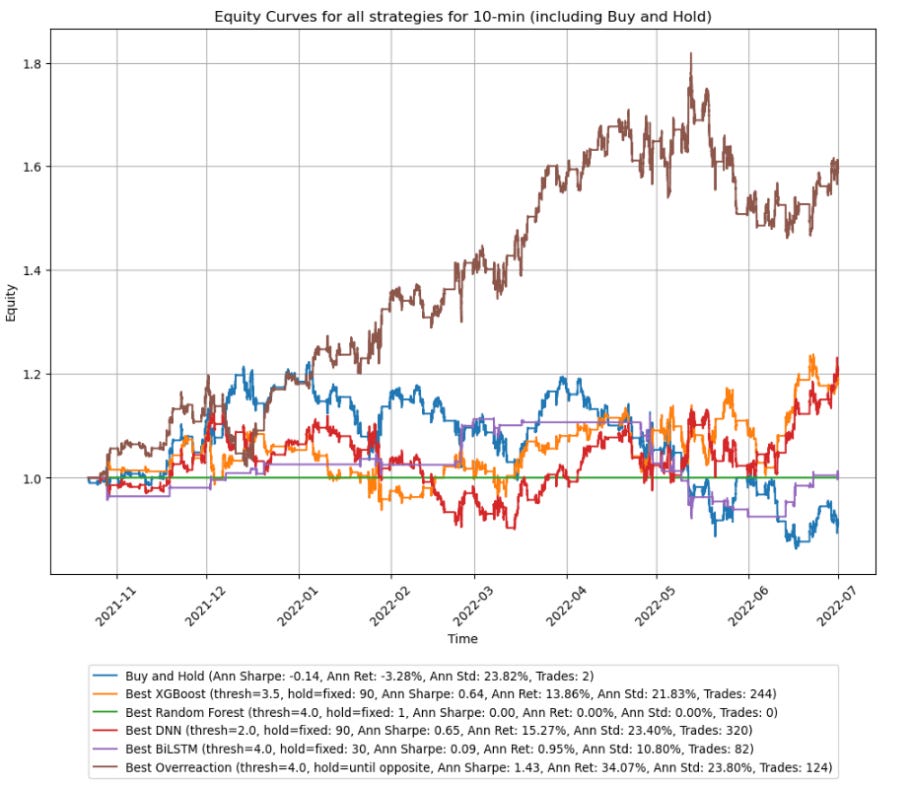

Machine learning models can systematically predict and monetize short-term market overreactions by integrating high-frequency emotional data from social media with price volatility signals.

In the messy world of intraday trading, markets often overextend themselves, creating brief windows where prices deviate from reality.

This research shows that by feeding a transformer-based “emotion” model a constant stream of Apple-related tweets, we can actually predict which of these price spikes will turn into profitable momentum.

While a simple overreaction rule often struggles with market noise, sophisticated models like XGBoost and neural networks excel at identifying the subtle interplay between volume, volatility, and specific feelings like fear or sadness.

Interestingly, the study found a “sweet spot” at the 10-minute frequency, where these behavioral patterns are most pronounced and tradable. As the paper concludes, “the predictive content of emotions is both statistically robust and economically actionable”.

Lis, Szymon and Ślepaczuk, Robert and Sakowski, Paweł, Overreaction as an Indicator for Momentum in Algorithmic Trading: A Case of AAPL Stocks (February 21, 2026). Available at SSRN: https://ssrn.com/abstract=6282099 or http://dx.doi.org/10.2139/ssrn.6282099

Monsoons & Stock Returns

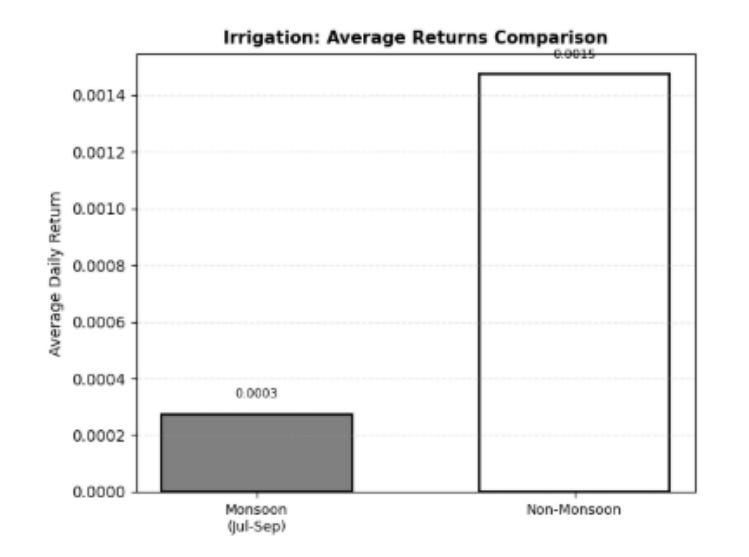

Abnormal rainfall during India’s monsoon season acts as a significant systematic shock to equity returns, with deficient rain specifically dragging down the performance of the banking and fast-moving consumer goods sectors.

In the Indian economy, the annual monsoon is far more than a weather event; it is a critical macroeconomic driver that dictates agricultural productivity and, by extension, rural demand.

This research demonstrates that the stock market is highly sensitive to rainfall departures from the long-term average, as the monsoon directly impacts corporate earnings and inflationary expectations. When rainfall is deficient, the resulting drop in rural income and rise in food prices create a “double whammy” for sectors like banking and consumer goods, which rely heavily on the health of the rural heartland.

Interestingly, the paper finds that the market’s reaction isn’t always immediate or perfectly efficient, suggesting that investors often struggle to price in the full impact of a bad season until the data becomes undeniable.

Pandey, Utkarsh and Obuobi, Andrews Kwame and Kumar Singh, Mayannk and Bhattacharyya, Ritabrata, Effects of Monsoon on Indian Stock Market (February 19, 2026). Available at SSRN: https://ssrn.com/abstract=6270578 or http://dx.doi.org/10.2139/ssrn.6270578

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.