Recent Academic Research

Adaptive mean reversion filters, the real risks of government debt, how foreign demand moves yields, and the cognitive bias behind value investing

Welcome back to another issue of Recent Academic Research! Let’s get into it.

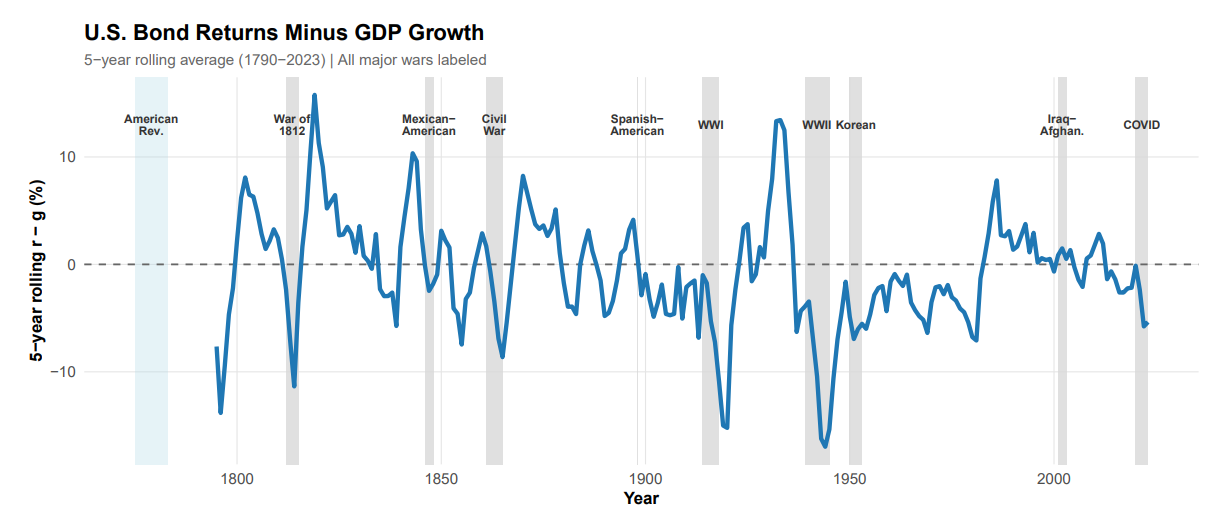

Government Bond Performance During Wars

History suggests that government debt is far from a safe haven during major geopolitical conflicts or pandemics.

We naturally assume that sovereign bonds offer absolute protection during times of extreme crisis. However, an analysis of centuries of financial data from the United States and the United Kingdom proves otherwise. During major wars and the recent pandemic, real returns on government bonds consistently collapsed and fell significantly below economic growth rates.

When nations face massive and unexpected spending needs, they rarely raise taxes enough to cover the bill (printing money is always the path of least resistance). Instead, governments quietly pass the cost onto bondholders through surprise inflation and financial repression policies that keep yields artificially low while purchasing power erodes.

Over a four year crisis window, these combined forces typically destroy about 31 percent of a bond portfolio's real value. As the authors conclude, "governments force bondholders to bear a substantial share of that fiscal burden" during these extreme spending shocks.

Zhengyang Jiang, Hanno Lustig, Stijn Van Nieuwerburgh, and Mindy Z. Xiaolan, “Are Government Bonds Safe in Times of War and Pandemic?,” NBER Working Paper 34820 (2026), https://doi.org/10.3386/w34820.

Financial Literacy and Dividend Anomaly

Does a basic misunderstanding of exponential math cause investors to chronically undervalue high yield dividend stocks?

The value premium found in high dividend stocks is one of the oldest anomalies in finance, but its root cause might simply be human cognitive limits. This research shows that investors broadly fail to grasp the mechanics of compound growth, leading them to severely underestimate the future value of reinvested dividends.

Using a global survey of financial literacy, the study proves that the dividend anomaly is wildly profitable in regions where the public struggles with compounding math. In these areas, the strategy generates nearly triple the returns compared to highly literate regions.

Because the average investor cannot intuitively model exponential growth, they simply refuse to pay a fair price for cash flow generating assets. The authors conclude that "our paper highlights financial education as a key tool for improving market efficiency."

Chen, Xin and yin, xueqian and Wang, Wei, Unveiling the Value Investing: The Crucial Role of Compound Rate Understanding. Available at SSRN: https://ssrn.com/abstract=6211283 or http://dx.doi.org/10.2139/ssrn.6211283

Advanced Filtering for Mean Reversion

A superior model to measure the mean-reverting capabilities of the underlying.

Mean reversion trading relies on the assumption that an asset will eventually return to its fair price after being pushed around by short term noise. The challenge is always defining that fair price. This research introduces a flexible filtering technique that acts as an intelligent smoothing tool.

By adjusting how much weight it gives to local price vol versus the bigger picture, the model extracts a cleaner signal of the true underlying trend. When the market behaves normally, the filter hugs the price closely.

Ultimately, this refined spread between the erratic spot price and the smooth latent fair value creates a highly measurable trading signal. As the authors state, this approach "expands the expressiveness of the kernel beyond simple exponential smoothing."

Xu, Zhichen and Firoozye, Nick and Koukorinis, Andreas and Treleaven, Philip and Zhu, Wilbur, Advanced Signal Filtering for Mean Reversion trading (February 12, 2026). Available at SSRN: https://ssrn.com/abstract=6225198

Interest Rates and Foreign Demand

Global investors seeking safe assets systematically drive down domestic real interest rates independently of local economic fundamentals.

We often attribute falling real interest rates to domestic forces like inflation expectations or monetary policy adjustments. This paper proves that foreign appetite for domestic Treasury securities plays a massive role in moving the market.

By tracking cross border capital flows, the research isolates the specific yield changes driven purely by international portfolio balancing rather than domestic news. When global uncertainty spikes, foreign capital floods into sovereign safe assets, pushing down yields regardless of what the local economy is doing (proving that domestic yields are often hostage to global anxieties).

The researchers conclude that "foreign demand is not a peripheral factor but a systematic contributor" rather than a temporary crisis anomaly.

Crooker, John, Global Portfolio Demand and the Dynamics of U.S. Real Interest Rates. Available at SSRN: https://ssrn.com/abstract=6211282 or http://dx.doi.org/10.2139/ssrn.6211282

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.