Recent Academic Research

Momentum in digital assets, AI equity valuations, bias in prediction markets, and volatility risk premia

Welcome back to another issue of Recent Academic Research! Let’s get into it.

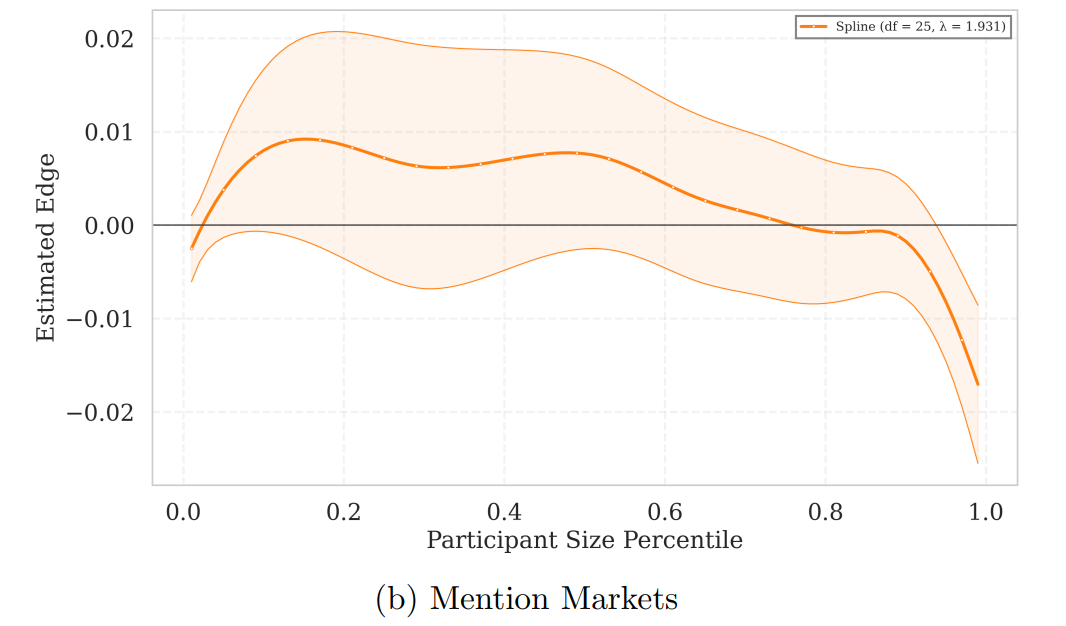

Bias in Prediction Markets

Prediction markets are frequently distorted by wealthy, ideological “whales” who overpay for their preferred outcomes, creating a profitable edge for smaller, more objective traders.

While many view prediction markets as great forecasting tools, this research shows they are often just mirrors of wishful thinking.

The study reveals that the biggest players in these markets, the “whales” who place the largest bets, are frequently the least sophisticated participants. Instead of trading on secret information, these high-stakes actors are typically driven by ideological conviction and a “Yes Bias,” which is the tendency to overpay for an event simply because they want it to happen.

This behavior creates a structural opportunity for smaller, disciplined traders to profit by taking the opposite side of these emotionally charged bets (as I currently am - more on that in this week’s paid post).

Furthermore, the data shows that the loudest participants in the comments are often the least informed, proving that social buzz is usually just distracting noise.

Deleep, Avaneesh and Lee, John and Bai, Jenny and Suresh, Dhruv and Dhawan, Harsh, How Wise is the Crowd? Bias and Edge in Prediction Markets (February 28, 2026). Available at SSRN: https://ssrn.com/abstract=6322678 or http://dx.doi.org/10.2139/ssrn.6322678

AI Productivity and Markets

Stock market gains from AI productivity breakthroughs are effectively “canceled out” by investors when political and economic uncertainty is high.

We often expect a major technological leap to drive stock prices up instantly, but this paper shows that the broader political climate acts as a gatekeeper. Since 2018, productivity gains in AI-intensive firms have triggered significant valuation jumps, but only when economic policy uncertainty was low.

When the news cycle is dominated by trade wars or election instability, these same productivity gains have almost no impact on stock prices. This happens because high uncertainty causes “risk premia” to spike, meaning investors demand a much higher discount to hold onto growth stocks, which masks the value of the actual technological progress.

For the market, this means that even the most revolutionary AI tools won’t move the needle if the macro environment is too volatile.

Oka, Arsene, Economic Policy Uncertainty and the Pricing of Productivity in AI Equities (February 21, 2026). Available at SSRN: https://ssrn.com/abstract=6283479 or http://dx.doi.org/10.2139/ssrn.6283479

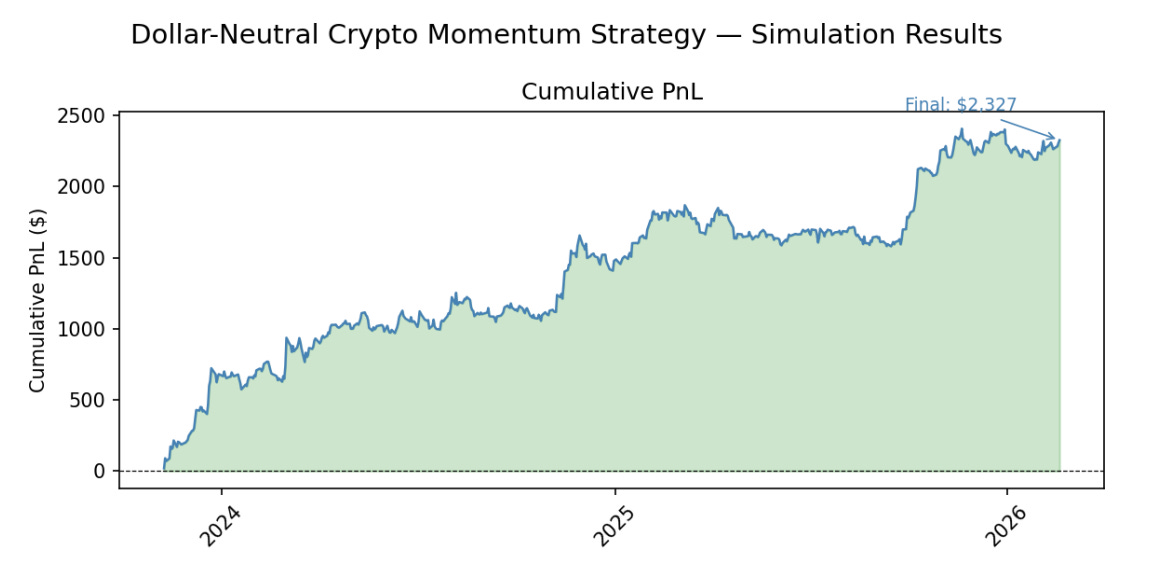

Momentum Strategy in Crypto

The cryptocurrency market is governed by a powerful momentum effect, where past winners consistently outperform laggards over a two-to-four-month horizon.

In the chaotic world of digital assets, many investors struggle to find a signal in the noise, but a simple momentum strategy proves remarkably robust.

By analyzing the 50 most active cryptocurrencies, this research demonstrates that coins with the strongest performance over the last 50 to 130 days tend to maintain their lead, while underperformers continue to slide.

This isn’t just a side effect of Bitcoin’s price movements; a market-neutral approach (buying the top winners and shorting the bottom losers) delivered double the risk-adjusted returns (Sharpe Ratio of 1.98) of a simple Bitcoin buy-and-hold strategy.

For investors, this finding proves that “systematic cross-sectional strategies offer a viable and risk-aware alternative to the directional speculation that dominates retail crypto trading.”

Chen, Kaston and Chen, Jaslyn, A Forecast Model For Crypto Currencies (February 24, 2026). Available at SSRN: https://ssrn.com/abstract=6300843 or http://dx.doi.org/10.2139/ssrn.6300843

Volatility as an Asset Class

Volatility should be treated as a standalone asset class that offers a consistent “insurance premium” to those willing to provide liquidity during market stress.

Most investors view volatility simply as a measure of risk, but successful funds treat it as a source of steady income, similar to collecting insurance premiums. This research highlights the “Volatility Risk Premium,” a structural reality where the market consistently overestimates how much stocks will actually swing, allowing option sellers to pocket the difference.

While this strategy provides steady “carry” or income, it comes with the risk of sudden, sharp losses during market crashes. To manage this, the paper suggests monitoring the “term structure” (the difference between short-term and long-term volatility expectations) as a warning sign to reduce exposure before a blow-up.

For a diversified portfolio, treating volatility as an asset is essential because “volatility exposure, managed with discipline, is one of the most powerful tools for navigating regime transitions.”

Verma, Divyanshu, Volatility as an Asset Class: Carry, Convexity, Crash Risk, and Hedge Fund Implementation (November 11, 2025). Available at SSRN: https://ssrn.com/abstract=6301718 or http://dx.doi.org/10.2139/ssrn.6301718

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.