Recent Academic Research

FX return relationship with macro announcements and Treasury auctions, a new trend following strategy, and seasonality in the mortgage markets

Effect of Macro News and Treasury Auctions

Foreign exchange returns spike when macroeconomic announcements follow Treasury auctions, revealing a powerful link between safe asset demand and currency markets.

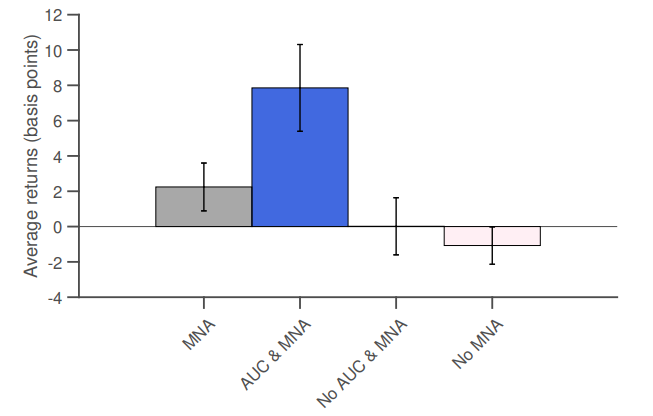

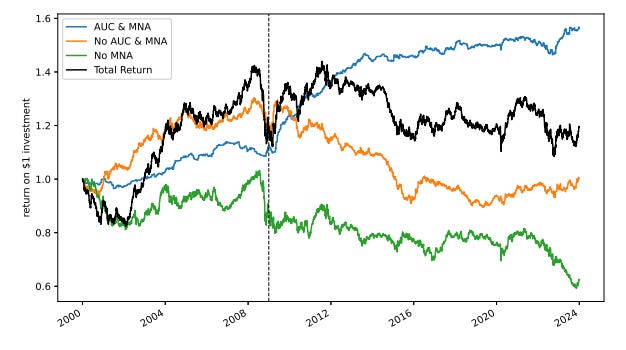

The paper shows that when macroeconomic announcements are immediately preceded by U.S. Treasury auctions, foreign currencies appreciate by nearly 8 basis points relative to the U.S. dollar, while on other announcement days, returns are negligible. This pattern is consistent across the G9 currencies, with the Swiss franc and Norwegian krone seeing the largest moves. The effect has persisted over the past two decades and is especially pronounced following the global financial crisis.

Importantly, this return pattern does not depend on the type of macro announcement (whether it’s GDP, CPI, or payrolls) or the maturity of the Treasury debt issued. The returns build gradually overnight before announcements and continue into the U.S. trading session, suggesting that these are not just quick reactions to the data but part of a broader dynamic.

The authors tie this pattern to shifts in Treasury demand. Primary dealers reduce their bids at auctions before major economic releases, constrained by risk limits. This reduction weakens Treasury demand and spills into FX markets, where the dollar depreciates as dealers adjust their positions. The effect strengthens when dealer balance sheets are more stretched, amplifying currency moves and trading volumes across markets.

Krohn, Ingomar and Vala, Rishi, Auctions, Announcements, and Abnormal Returns (April 06, 2025). Available at SSRN: https://ssrn.com/abstract=5207418 or http://dx.doi.org/10.2139/ssrn.5207418

Risk-Adjusted Trend Following

This study presents a simple trend-following strategy with a Sharpe ratio of 1.06 and a max drawdown nearly half that of the S&P 500.

The authors present a strategy that begins by calculating each stock’s excess return relative to its variance (essentially, its market-implied risk-adjusted return) over the past year. Only stocks with positive values are selected, forming a diverse candidate pool. The portfolio weights are then optimized daily using mean-variance optimization, balancing expected returns against estimated covariance while capping any single stock’s weight at 10% for diversification.

If the broader market (measured via SPY) shows negative excess return over the prior year, the strategy moves fully to cash. A final filter applies moving averages: positions are held only if the stock’s current price stays above its short-term average, which itself must be above the long-term average, effectively ensuring positions align with prevailing trends.

The performance tells the story. From 2014 to 2025, the strategy outpaces the S&P 500, growing nearly 25-fold while keeping risk in check. The Sharpe ratio reaches 1.06, compared to 0.69 for the index, and the strategy’s worst drawdown is just 17.1%, nearly half the market’s. Even after accounting for trading costs, the strategy’s outperformance persists.

Liu, Shitao, Ride the Right Horse: a Systematic Trend Strategy for Superior Return Using Portfolio Utility Optimization (March 22, 2025). Available at SSRN: https://ssrn.com/abstract=5189974 or http://dx.doi.org/10.2139/ssrn.5189974

Mortgage Application and Default Seasonality

Mortgage lenders are more likely to deny refinance applications and make riskier loans when homebuying season peaks.

This paper explores how seasonal fluctuations in mortgage demand impact lenders’ behavior. Using nationwide mortgage application data, the authors show that lenders face capacity constraints during the spring and summer months, when home purchase applications surge.

As a result, they ration credit, not just for homebuyers, but also for homeowners seeking to refinance. Refinancing denial rates rise by nearly half a percentage point when purchase loan demand increases by 10 percent.

The boxplot of seasonal factors reveals clear peaks in mortgage demand from March to June, followed by sharp declines in winter. These capacity pressures also affect loan quality. Loans originated during these high-demand months exhibit higher default rates within three years, even after accounting for borrower credit characteristics and loan terms.

This suggests that overworked loan officers make weaker underwriting decisions under time pressure. The findings imply that the cyclical nature of the housing market not only shapes access to credit but also subtly affects financial stability.

Jo, Young and Liu, Feng, Mortgage Seasonality, Capacity Constraints, and Lender Responses (April 18, 2025). Consumer Financial Protection Bureau Office of Research Working Paper No. 25-04, Available at SSRN: https://ssrn.com/abstract=5222368 or http://dx.doi.org/10.2139/ssrn.5222368

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

I would love to see the second strategy coded up.