Recent Academic Research

A new paper from Nassim Taleb, high equity valuations, global power and market returns, and valuation multiples.

Welcome back to another issue of Recent Academic Research! Let’s get into it.

U.S. Equity Valuations

Does the decline of the labor share mean the stock market isn’t actually expensive?

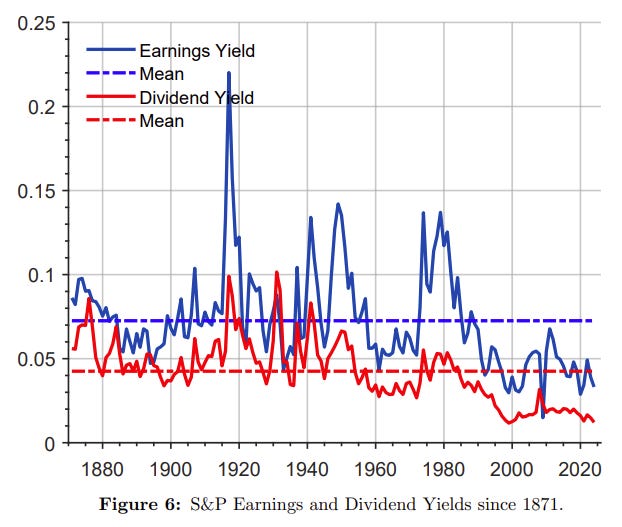

Traditional valuation metrics have signaled an overheated U.S. market for nearly 30 years, yet the expected mean reversion has failed to materialize. By shifting the lens from standard accounting to macroeconomic data, researchers found that while the "earnings yield" has plummeted, the "free cash flow yield" has remained remarkably stable around its historical mean of 3.6%.

This divergence is mechanically driven by two factors: a significant drop in the share of corporate output paid to labor and a lack of significant growth in measured corporate investment.

Effectively, corporations are generating more cash for owners without needing to reinvest it into physical capital, a shift that makes the market look expensive on paper while the underlying cash flows remain grounded. This suggests that "low" earnings yields might be a permanent fixture of the modern economy rather than a bubble waiting to burst. As the authors note, "persistently low earnings yields need not reflect mispricing".

Atkeson, Andrew, Jonathan Heathcote, and Fabrizio Perri. “A Macroeconomic Perspective on Stock Market Valuation Ratios.” Staff Report 682. Federal Reserve Bank of Minneapolis, January 2026. https://doi.org/10.21034/sr.682.

Geopolitical Power and Market Returns

Can the geopolitical strength of a nation predict how closely its stock market moves with the world?

While investors often look to local volatility or GDP to explain market co-movements, a new study suggests that a nation's "Global Power" is a primary driver of financial integration. Using an index that combines military, political, and economic strength, researchers discovered that as a country's global power increases, its stock market becomes significantly more correlated with other G20 nations.

This relationship likely stems from the fact that powerful nations exert more influence over global trade policies and international agencies, which in turn shapes the risk premiums and returns for their domestic firms.

The findings indicate that shifts in the global order, such as the rising power of China and the relative decline of the US, directly impact the diversification benefits available to international investors.

Gupta, Rakesh and Haddad, Sama and Selvanathan, E. A., Global Power and Stock Market Co-Movements: A Study of G20 Markets (July 15, 2024). Available at SSRN: https://ssrn.com/abstract=6236638

Extreme Valuation Multiples

Should you stop worrying about valuation multiples when they are in the middle of the pack?

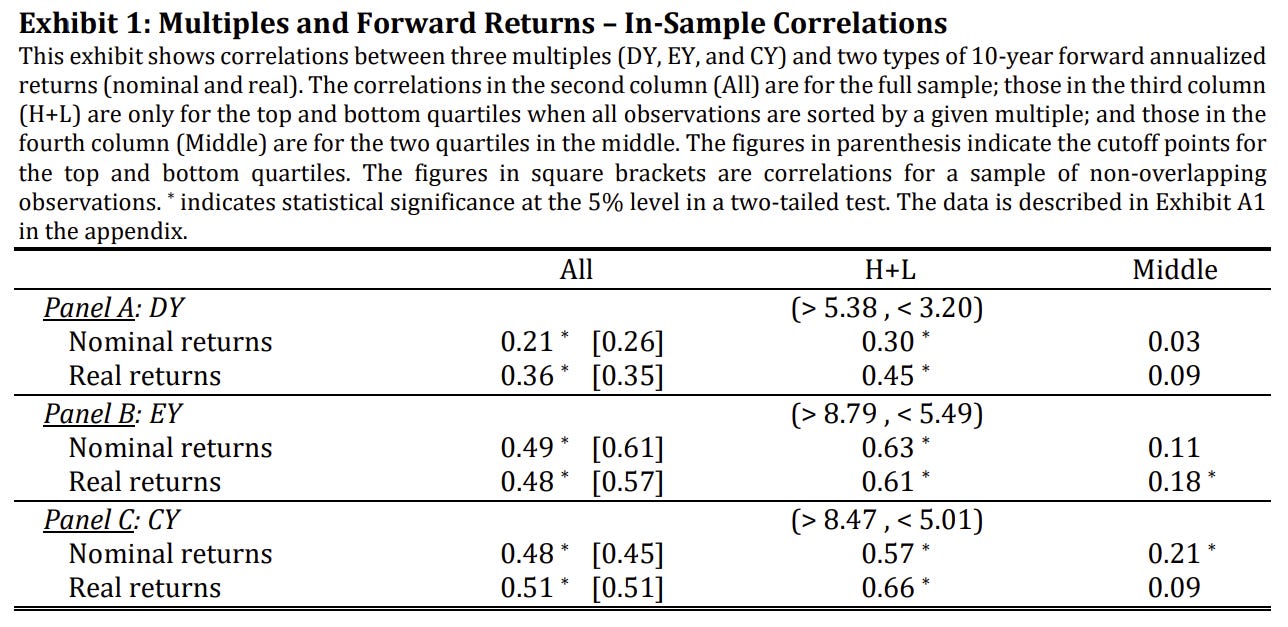

Market multiples like the dividend yield or CAPE are famous for forecasting long-term returns, but their predictive power isn’t constant across all levels. New evidence shows that these metrics are far more useful when they are at historical extremes, specifically in the top or bottom quartiles of their range.

When multiples are in the “middle,” the relationship to future returns effectively breaks down, providing almost no actionable signal for investors.

A dividend yield only provides a strong signal when it is roughly below 3% or above 6%, whereas the “middle” range fails to convey meaningful information about future market performance. As the research highlights, “multiples are far more useful when they are relatively high or low”.

Estrada, Javier, Multiples for Valuation: Go High, Go Low, Ignore the Middle (February 01, 2026). Available at SSRN: https://ssrn.com/abstract=6152048

Taleb’s Newest Paper

Are American options providing a layer of “hidden” protection that your pricing model is missing?

Conventional pricing systems often treat interest rates as fixed inputs, a simplification that systematically underestimates the value of the early-exercise feature in American options. By introducing randomness into funding and dividend rates, this research (by Nassim Taleb!) develops a framework to quantify “unaccounted optionality” that remains invisible to standard risk systems.

The study highlights that the American contract acts as a “smart” instrument, adapting its exercise timing to benefit from transient peaks in the interest rate differential or unexpected market squeezes.

This flexibility provides a crucial lower bound against adverse movements, effectively acting as an option on the funding environment itself. This feature “embodies an additional, often unrecognized, layer of convexity”.

Hassan, Noura El, Bacel Maddah, and Nassim N. Taleb. "Hidden Risks and Optionalities in American Options." arXiv preprint arXiv:2602.14350 (2026).

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.