Recent Academic Research

The relationship between Wikipedia page views for public companies and their future stock returns, media tone's effect on currency markets, and the consequences of portfolio rebalancing

Welcome back to another issue of Recent Academic Research! This week includes a couple of relevant charts from the academic papers themselves. Let me know if you all like this format!

Let’s get into it.

Wikipedia Page Views and Stock Performance

Investor attention has long been studied using proxies like Google searches and Twitter activity, but this paper explores an underutilized source: Wikipedia page views. By analyzing changes in Wikipedia traffic for publicly traded firms, the study investigates whether this metric can serve as a signal for stock performance. Using data from October 2016 to December 2023, the author examines industry trends, stock characteristics, and the profitability of trading strategies based on Wikipedia view trends. The study also tests long-short portfolios formed by sorting stocks into terciles based on changes in Wikipedia views and evaluates their performance against common risk models.

Findings:

Firms in the telecommunications, consumer durables, and high-technology sectors experience the highest increases in Wikipedia page views, indicating heightened investor attention.

Stocks with rising Wikipedia page views tend to have higher returns, lower earnings per share (EPS), and higher price-to-earnings (P/E) ratios, suggesting a growth-oriented investor preference.

A monotonic relationship exists between Wikipedia view increases and stock performance: firms in the highest tercile of view increases exhibit the highest equal-weighted and value-weighted returns.

A long-short strategy (going long on stocks with the highest Wikipedia view increases and shorting those with the lowest) yields positive abnormal returns, outperforming standard benchmarks.

A variant of this strategy, where the short position is replaced with an S&P 500 short, delivers even higher returns but exhibits greater volatility.

Factor model regressions show that Wikipedia-based portfolios generate statistically significant alphas, indicating that the excess returns are not explained by common risk factors like market exposure, size, value, or momentum.

Weekly portfolio rebalancing outperforms monthly rebalancing, suggesting that investor attention effects captured by Wikipedia views are short-term in nature.

These results suggest that Wikipedia page views act as a valuable proxy for investor attention, offering predictive power for stock returns. The observed effect is likely driven by increased interest from retail investors, particularly in high-growth sectors.

Pyun, Chaehyun, The Wikipedia Effect: Analyzing Investor Attention for Strategic Investment Decisions (April 30, 2024). Economics Letters, volume 241, 2024[10.1016/j.econlet.2024.111836], Available at SSRN: https://ssrn.com/abstract=5172055 or http://dx.doi.org/10.2139/ssrn.5172055

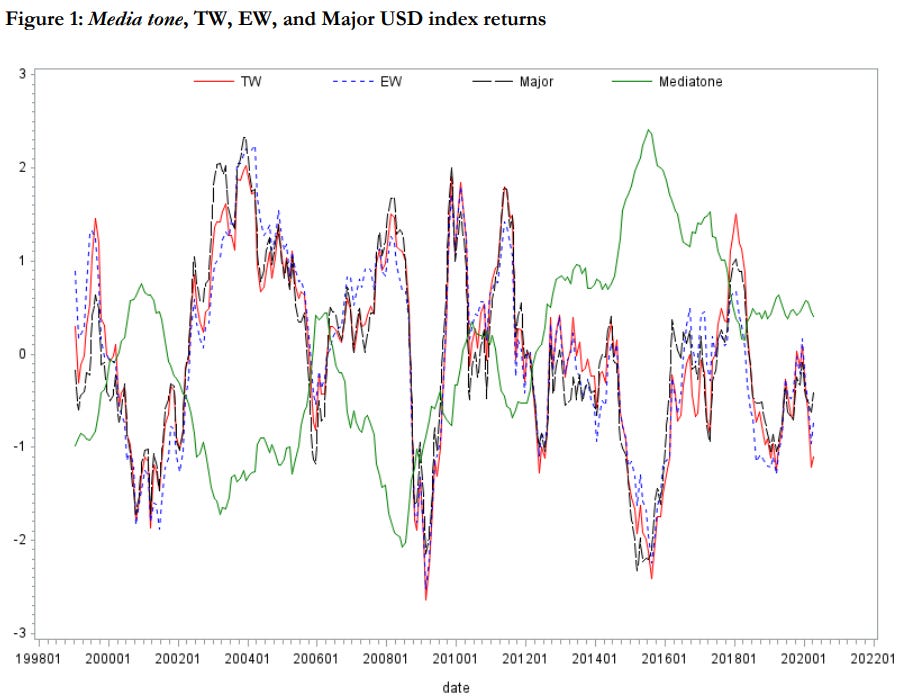

Media Tone and Currency Markets

The study investigates whether media sentiment about the U.S. dollar influences currency market returns. Drawing from existing literature on sentiment-driven asset pricing, the authors construct a Media Tone Index using text-based sentiment analysis of financial news. They test whether this measure is a systematic risk factor in exchange rate movements. The methodology involves regression analysis of excess currency returns against the Media Tone Index, controlling for known risk factors.

Findings:

Media sentiment predicts currency returns: A more positive media tone on the U.S. dollar correlates with higher future returns on trade-weighted and major USD indices.

Media tone influences risk premia: Currencies more sensitive to U.S. media tone earn higher risk-adjusted returns, implying that sentiment is a priced factor.

Impact is strongest for trade-weighted indices: The effect is most pronounced in the trade-weighted (TW) and equally weighted (EW) USD indices, rather than individual currency pairs.

Persistence and economic significance: The predictive power of media tone persists across different model specifications and time periods.

Market reactions align with behavioral finance theories: Investors likely respond to media sentiment shifts, creating return predictability in currency markets.

Heimonen, Kari and Lehkonen, Heikki and Pukthuanthong, Kuntara, Media tone is a priced risk factor in currency markets (March 07, 2025). Available at SSRN: https://ssrn.com/abstract=5170200 or http://dx.doi.org/10.2139/ssrn.5170200

The Effects of Portfolio Rebalancing

Portfolio rebalancing is a common practice among institutional investors, but its unintended effects on asset prices are not widely understood. This paper explores how predictable rebalancing flows impact market returns and how traders can exploit these patterns to generate excess returns. By analyzing index fund rebalancing activities and investor flows, the authors uncover systematic price pressures that arise due to mechanical rebalancing strategies.

Findings:

Institutional rebalancing creates predictable demand shocks in financial markets, leading to temporary price distortions.

Traders can “front-run” these rebalancing flows by anticipating and exploiting the price impact before it occurs.

A simple trading strategy that front-runs institutional rebalancing yields significantly higher cumulative returns than a passive S&P 500 investment, even after adjusting for volatility.

The rebalancing-induced price effects are strongest around quarter-end and year-end, when many funds adjust their portfolios.

Market impact is asymmetric: large purchases drive prices up more than large sales drive them down, leading to short-term momentum effects.

Liquidity constraints amplify price dislocations, creating opportunities for informed traders to profit from temporary mispricings.

These findings highlight how seemingly benign portfolio rebalancing strategies can have unintended consequences, distorting asset prices and creating exploitable inefficiencies.

NBER Working Paper Series. Campbell R. Harvey, Michele G. Mazzoleni & Alessandro Melone. The Unintended Consequences of Rebalancing. March 2025. National Bureau of Economic Research, 1973.

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

Nice post.

The Wikipedia numbers would be very easy to manipulate. Getting page views on a particular webpage is a trivial exercise and not that expensive so I wonder whether in this case you might be able to get the tail to wag the dog.

This looks like an interesting divergence

Would like to see more details on the methodology behind these cumulative gains